By Encore Events Global | Published: March 2026 | Category: Corporate MICE & Event Finance | Read Time: 12 min

If you have ever managed the post-event finance reconciliation for a large corporate offsite, you already know the pain. Invoices from 20 different vendors. Five different GST rates. Three vendors without proper GST registration. Two international suppliers with no Indian tax documentation at all. And your finance team asking why the Input Tax Credit claim does not match the books.

This is not an edge case. This is the standard reality of corporate event finance management in India — and it is entirely avoidable.

Single-Window Billing is the structural solution to this problem. This article explains exactly what it is, why GST compliance in events is uniquely complex, and why your procurement and finance teams should make it a non-negotiable requirement in every event management RFP you issue from today.

Pro Tip: Forward this article to your CFO, Procurement Head, or Finance Controller before your next event RFP. The GST implications of multi-vendor event billing are significant — and most organizations discover them only after the event is over.

1. Why Event GST Compliance is Uniquely Complex

Corporate event management sits at the intersection of multiple GST categories simultaneously. Unlike procuring a single product or service — where one GST rate applies cleanly — a corporate event involves a basket of services, each governed by different HSN/SAC codes, different GST rates, and different compliance requirements.

Consider a standard 3-day corporate offsite for 300 delegates. The procurement involves all of the following service categories in a single event:

| Service Category | GST Rate | SAC Code | ITC Eligibility |

|---|---|---|---|

| Hotel Accommodation | 12% (tariff INR 1,000–7,500) or 18% (above INR 7,500) | 9963 | Eligible with conditions |

| Food & Beverage (Catering) | 5% (without ITC) or 18% (with ITC) | 9963 | Partially restricted |

| Transportation (Coach / Bus) | 5% (without ITC) or 12% (with ITC) | 9964 | Eligible with conditions |

| AV & Technical Production | 18% | 9987 | Eligible |

| Event Management Services | 18% | 9983 | Eligible |

| Mandap / Venue Decoration | 18% | 9997 | Eligible |

| Photography & Videography | 18% | 9981 | Eligible |

| Entertainment / Performer Fees | 18% | 9996 | Eligible |

| Printing & Branding Materials | 12% or 18% | 9989 | Eligible |

| Air Travel (Domestic) | 5% (Economy) or 12% (Business) | 9964 | Eligible |

Each of these services comes from a different vendor. Each vendor issues a separate invoice. Each invoice has its own GST number, its own HSN/SAC code, its own payment terms — and its own potential for error, non-compliance, or missing documentation.

This is why event GST compliance is not a simple accounting task. It is a multi-layered tax management exercise — and most corporate procurement teams are not equipped to handle it efficiently without structural support.

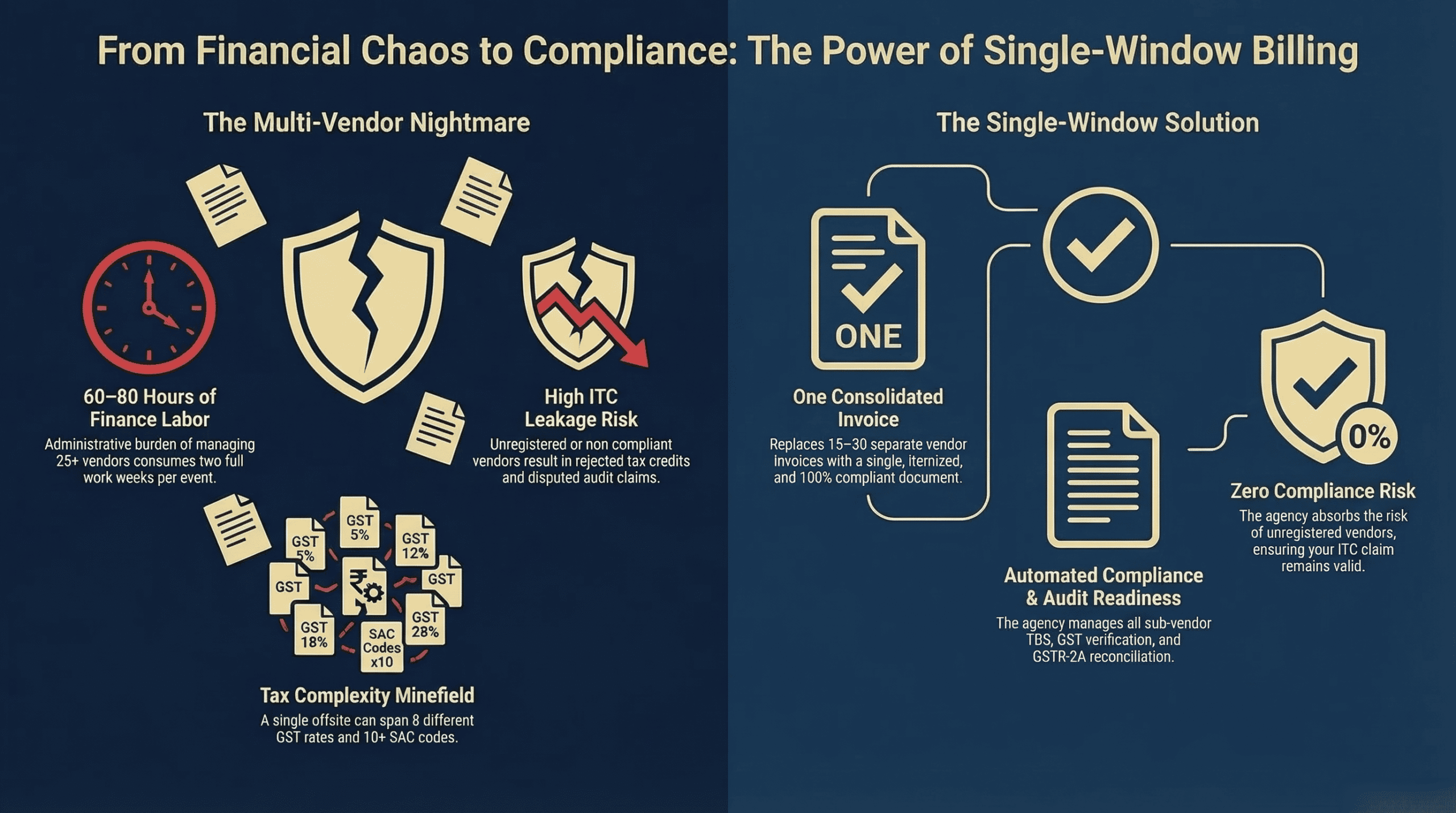

Key Insight: A single corporate offsite can generate invoices spanning 6 to 8 different GST rates and 10+ different SAC codes. Without a consolidated billing structure, your finance team is essentially managing a mini tax audit for every event.

2. The Multi-Vendor Billing Problem: What Actually Happens

When a corporate organization manages event vendor payments directly — without a Single-Window Billing structure — the following sequence of problems almost always unfolds.

Problem 1: Invoice Avalanche

Your accounts payable team receives 15 to 30 separate invoices after the event. Each requires individual vendor verification, PO matching, GST validation, and payment processing. For a finance team managing hundreds of vendor relationships, each event adds a disproportionate administrative burden.

Problem 2: Unregistered or Non-Compliant Vendors

Many event sub-vendors — local decorators, small transport operators, regional entertainers, freelance photographers — operate below the GST registration threshold or are not GST-registered at all. When you pay them directly, you lose ITC eligibility on those amounts entirely. Worse, if these vendors have provided incorrect GSTIN numbers, your ITC claim can be rejected during a GST audit.

Problem 3: Mismatched GSTR-2A Reconciliation

For ITC claims to be valid, the GST paid on vendor invoices must appear in your GSTR-2A (auto-populated from supplier filings). If any vendor files their GSTR-1 late, incorrectly, or not at all, your ITC claim becomes disputed — even though you paid the tax. This is a compliance risk that multiplies with every additional vendor in the chain.

Problem 4: TDS Complexity

Many event vendors — particularly performers, celebrities, and professional service providers — are subject to TDS deduction under Section 194C or 194J of the Income Tax Act. When your organization pays these vendors directly, TDS compliance becomes your responsibility. Missed TDS deductions create disallowance risks during income tax assessments.

Problem 5: Multi-State GST Complications

For offsites held outside your company’s home state — for example, a Mumbai-based company holding an offsite in Goa — inter-state GST (IGST) rules apply for certain services. Managing IGST vs CGST/SGST distinctions across 20+ vendors in a different state is a compliance minefield for most corporate finance teams.

Real Cost of Multi-Vendor Billing: In a typical 500-delegate offsite with 25 vendors, the administrative cost of managing individual invoices, GST reconciliation, TDS compliance, and payment processing can consume 60 to 80 hours of your finance team’s time — equivalent to 2 full working weeks for one person.

3. What is Single-Window Billing?

Single-Window Billing is a financial model in which your event management agency acts as the single billing entity for all event-related services. Instead of receiving separate invoices from every sub-vendor — the hotel, the transport company, the AV team, the caterer, the decorator, and all others — you receive one consolidated, fully itemized, 100% GST-compliant invoice from your event management agency.

The event management agency handles all sub-vendor payments, GST compliance, TDS deductions, and reconciliation on your behalf. Your organization’s financial relationship is exclusively with one entity.

Single-Window Billing vs Traditional Multi-Vendor Billing

| Parameter | Traditional Multi-Vendor Billing | Single-Window Billing |

|---|---|---|

| Number of invoices | 15 – 30 per event | 1 per event |

| GST compliance responsibility | Your finance team | Event management agency |

| ITC claim complexity | High — multiple vendors, rates, SAC codes | Low — single invoice, single ITC claim |

| TDS management | Your accounts team per vendor | Agency handles all sub-vendor TDS |

| GSTR-2A reconciliation risk | High — dependent on all vendors filing correctly | Low — single supplier relationship |

| Unregistered vendor risk | High — you absorb the ITC loss | Zero — agency absorbs and manages |

| Finance team hours per event | 60 – 80 hours | 4 – 6 hours |

| Vendor payment follow-up | Your team chases 20+ vendors | Zero — agency manages all payments |

| Audit readiness | Complex — requires 20+ vendor files | Simple — single invoice package |

4. How Single-Window Billing Works: Step by Step

Understanding the mechanics of Single-Window Billing helps your procurement team structure the right contractual relationship with your event management agency from the outset.

- Event Brief & Cost Proposal: Your organization issues an event brief. The agency prepares a fully itemized cost proposal breaking down every service category — accommodation, transport, production, F&B, entertainment — with individual line-item costs and applicable GST rates clearly shown.

- Single Contract Execution: You sign one master service agreement with the event management agency. The agency then contracts independently with all sub-vendors on your behalf.

- Advance Payment Structure: You make advance payments to the agency against a single GST-compliant invoice. The agency manages all sub-vendor advance payments from this pool.

- Sub-Vendor GST Verification: The agency verifies the GST registration status of every sub-vendor before engagement. Non-registered vendors are either replaced with compliant alternatives or their costs are restructured to protect your ITC eligibility.

- Event Execution & Cost Tracking: During the event, the agency tracks all actual expenditure against the approved budget in real time. Any variation is flagged and approved before being incurred.

- Post-Event Reconciliation: Within 7 to 10 working days after the event, the agency provides a complete cost reconciliation showing actuals vs estimates, with all supporting sub-vendor invoices available for your audit review.

- Final Consolidated Invoice: You receive one final GST-compliant invoice for the total event cost, inclusive of the agency’s transparent management fee, with ITC-eligible amounts clearly identified.

- GST Filing Support: The agency ensures all GST is filed correctly on their end so your GSTR-2A reflects the full input tax credit you are entitled to claim.

Encore Events Global Practice: Every event we manage is billed through a single, fully itemized invoice. Our management fee is shown as a separate line item — never buried in vendor costs. Every sub-vendor invoice is available for client audit review within 10 working days of event closure. Transparent billing is not a feature for us — it is a founding principle.

5. GST Rates Applicable to Corporate Event Services in India

Understanding the applicable GST rates across event service categories helps your finance team validate invoices and plan ITC claims accurately. The following is a comprehensive reference guide for corporate event procurement teams.

| Service | GST Rate | SAC Code | Notes |

|---|---|---|---|

| Event Management Services | 18% | 998590 | Applies to agency management fees |

| Hotel Accommodation (tariff up to INR 7,500/night) | 12% | 996311 | ITC available for business purposes |

| Hotel Accommodation (tariff above INR 7,500/night) | 18% | 996311 | ITC available for business purposes |

| Restaurant / Catering (AC restaurant) | 5% (no ITC) or 18% (with ITC) | 996331 | Caterer must opt for 18% to pass ITC |

| Outdoor Catering | 18% | 996334 | ITC eligible |

| Passenger Transport (road, contracted) | 5% or 12% | 996412 | 12% if ITC availed by transporter |

| Air Transport (Economy class) | 5% | 996411 | ITC eligible |

| Air Transport (Business class) | 12% | 996411 | ITC eligible |

| Sound, Lighting & AV Equipment Rental | 18% | 997319 | ITC eligible |

| Stage & Fabrication Services | 18% | 995468 | ITC eligible |

| Photography & Videography | 18% | 998981 | ITC eligible |

| Printing & Stationery | 12% or 18% | 998912 | Depends on product type |

| Artist / Performer Fees | 18% | 999619 | TDS also applicable under Sec 194J |

| Security Services | 18% | 998521 | ITC eligible |

| Manpower / Staffing Services | 18% | 850000 | ITC eligible if for business use |

Important Disclaimer: GST rates and SAC codes are subject to change based on GST Council notifications. The rates above reflect the position as of early 2026. Always verify current rates with your chartered accountant or tax consultant before finalizing event budgets and ITC claims.

6. Input Tax Credit (ITC): What You Can and Cannot Claim

Input Tax Credit is the mechanism by which businesses recover the GST paid on business inputs against their GST liability on outputs. For corporate events, ITC eligibility is not uniform — it depends on the nature of the event, the service category, and how the expense is classified in your books.

ITC Eligibility Framework for Corporate Events

| Event Type / Expense Category | ITC Eligibility | Reason |

|---|---|---|

| Business conference / strategy meeting | ✅ Eligible | Direct business purpose, not personal consumption |

| Product launch event | ✅ Eligible | Marketing and business promotion expense |

| Dealer / channel partner meet | ✅ Eligible | Business promotion, not personal entertainment |

| Training and development summit | ✅ Eligible | Employee development, business purpose |

| Annual general meeting (AGM) | ✅ Eligible | Statutory business requirement |

| Employee recreation / team outing | ❌ Blocked under Sec 17(5) | Classified as personal consumption / entertainment |

| Food & beverages (catering) | ⚠️ Restricted | Blocked under Sec 17(5)(b) unless obligatory under law |

| Accommodation for employees | ⚠️ Conditional | Eligible if for business purpose, documentation required |

| Outdoor catering at business event | ⚠️ Disputed | Subject to interpretation — consult CA for position |

| Gifts and mementos for delegates | ❌ Blocked | Gifts above INR 50,000 per person blocked under Sec 17(5)(h) |

The Critical Documentation Requirement

Even for ITC-eligible event expenses, the GST department requires robust documentation to substantiate claims during audits. Your event management agency’s Single-Window Invoice must be supported by the following documentation package:

- Original tax invoice from the event management agency with correct GSTIN, SAC code, and event details.

- Event purpose documentation — board approval, business justification, or internal event brief confirming the commercial purpose.

- Delegate list confirming attendance is business-related (employees, clients, dealers — not family members or personal guests).

- Payment proof — bank transfer records matching invoice amounts.

- Sub-vendor invoice summary available from the agency for audit reference.

Encore Events Global Practice: For every event we manage, we provide clients with a complete ITC documentation package within 10 working days of event closure. This includes the consolidated tax invoice, sub-vendor summary, SAC code mapping, and a reconciliation statement — everything your finance team needs for a clean ITC claim and audit-ready files.

7. The Finance Team’s Nightmare: Real Scenarios Without Single-Window Billing

The following scenarios are composite examples drawn from the real-world event billing challenges that corporate finance teams routinely face when events are managed without a Single-Window Billing structure.

Scenario 1: The Missing GSTIN

A pharmaceutical company organizes a 400-delegate medical conference in Hyderabad. The event involves 22 vendors. Three weeks after the event, the finance team discovers that 4 vendors — including the primary decorator and one of the transport operators — have provided incorrect or unverifiable GSTIN numbers. The GST paid on these invoices (approximately INR 3.2 lakh) cannot be claimed as ITC. The GSTIN errors were only discovered during GSTR-2A reconciliation — too late to replace the vendors or restructure the invoices.

Scenario 2: The Composite Supply Confusion

A banking sector company holds a 3-day leadership offsite at a resort in Lonavala. The resort bundles accommodation, meals, and conference hall rental into a single package rate and issues one invoice at 18% GST on the full amount. However, the finance team’s CA argues that meals should have been billed at 5% separately, making the composite invoice incorrectly structured. The resort refuses to reissue the invoice. The company faces an ITC reconciliation dispute for INR 6.8 lakh during their annual GST audit.

Scenario 3: The Late Filing Cascade

A manufacturing company manages a 250-delegate dealer meet directly with 18 vendors. Seven of the vendors — mostly smaller regional suppliers — file their GSTR-1 returns late or with errors. The company’s GSTR-2A does not reflect the GST paid on these invoices for the relevant quarter. The company files their ITC claim in good faith but receives a notice from the GST department asking them to reverse INR 4.5 lakh of ITC due to supplier filing mismatches. Recovering this requires follow-up with each vendor individually — a process that takes 4 months and significant legal correspondence.

Scenario 4: The International Artist TDS Disaster

A technology company books an international DJ for their annual employee celebration at INR 18 lakh. The payment is made directly by the company’s accounts team to the artist’s Indian booking representative. The TDS obligation under Section 194J (at 10%) was not deducted at the time of payment. During a tax assessment, the income tax department disallows the full INR 18 lakh expense as a deductible business expense due to TDS non-compliance — costing the company significantly more than the original TDS amount would have been.

Common Thread: In every scenario above, the root cause is the same — direct multi-vendor payment without a structured compliance layer between the corporate client and the event supply chain. Single-Window Billing eliminates this exposure entirely by making the event management agency the responsible billing and compliance entity.

8. Single-Window Billing for International Events: The Forex Dimension

For corporate offsites held outside India — in destinations like Dubai, Bangkok, Singapore, or Baku — the billing complexity multiplies significantly. In addition to GST management, your finance team now faces foreign exchange risk, cross-border payment compliance, and FEMA (Foreign Exchange Management Act) considerations.

International Event Billing Challenges Without Single-Window Structure

- Multi-currency invoices: Hotel invoices in AED, transport in THB, entertainment in USD — your accounts team manages exchange rate risk on each individual payment.

- Foreign vendor TDS: Payments to foreign vendors may attract TDS under Section 195 of the Income Tax Act. Each payment requires a CA certificate or Lower Deduction Certificate — multiplied across every vendor.

- FEMA compliance: Outward remittances for event services require proper documentation under FEMA. Each individual vendor payment needs separate Form 15CA/15CB filings.

- No GST ITC on foreign services: Services consumed outside India are not eligible for Indian GST ITC. However, the Indian event management fee component is — and this must be correctly segregated in the billing.

- Exchange rate reconciliation: If 15 vendors are paid at different exchange rates on different dates, the final cost reconciliation against your INR budget becomes a complex accounting exercise.

How Single-Window Billing Solves the International Dimension

| Challenge | Without Single-Window | With Single-Window Billing |

|---|---|---|

| Foreign currency payments | Your team manages 15+ forex transactions | Agency manages all forex, you pay in INR |

| Exchange rate risk | Spread across multiple payment dates | Single exchange rate agreed at contract stage |

| FEMA compliance | Multiple Form 15CA/15CB filings required | Single outward remittance, agency handles rest |

| Foreign vendor TDS | Your CA must assess each vendor payment | Agency manages all foreign vendor tax compliance |

| Budget reconciliation | Complex multi-currency reconciliation | Single INR invoice with full cost breakdown |

| GST on Indian services component | Difficult to segregate from foreign costs | Clearly separated in single invoice structure |

9. What to Look for in an Event Agency’s Billing Model

Not all event management agencies that claim to offer Single-Window Billing actually deliver it in a way that meets corporate GST compliance standards. Here is a precise checklist for your procurement team to evaluate an agency’s billing model before awarding a contract.

The 10-Point Billing Compliance Checklist

| # | Requirement | Why It Matters | How to Verify |

|---|---|---|---|

| 1 | Agency has valid GST registration | Foundation of compliant billing | Verify GSTIN on GST portal |

| 2 | Invoice shows SAC code for each service line | Required for correct ITC classification | Request sample invoice before contract |

| 3 | Management fee shown as separate line item | Prevents hidden markups, enables clean ITC | Insist on itemized quote structure |

| 4 | Sub-vendor GST verification process exists | Protects your ITC from non-compliant vendors | Ask for agency’s vendor onboarding SOP |

| 5 | Post-event sub-vendor invoice summary provided | Supports ITC documentation and audit readiness | Request sample post-event reconciliation report |

| 6 | TDS compliance handled for applicable vendors | Prevents TDS disallowance risk on your books | Confirm in contract terms |

| 7 | GSTR-1 filing timeliness track record | Ensures your GSTR-2A reflects ITC on time | Ask for reference from past corporate clients |

| 8 | Forex management for international events | Reduces exchange rate risk and FEMA complexity | Ask for international event billing sample |

| 9 | Event purpose documentation support | Strengthens ITC claim substantiation | Confirm agency provides event brief documentation |

| 10 | CA-reviewed billing process | Ensures overall GST compliance integrity | Ask if agency’s billing is reviewed by a qualified CA |

Red Flag to Watch: If an event agency cannot provide a sample post-event reconciliation report or refuses to show management fees as a separate line item — walk away. These are not optional transparency features. They are the basic minimum of a GST-compliant billing relationship.

10. Frequently Asked Questions

Q1: Can a company claim ITC on corporate event expenses in India?

Yes, companies can claim ITC on corporate event expenses, subject to conditions. ITC is available when the event has a clear business purpose — such as a product launch, dealer meet, business conference, or training summit. ITC is blocked under Section 17(5) of the CGST Act for expenses related to personal consumption, employee recreation, or events that are not directly linked to business activities. Food and beverage costs are generally restricted under Section 17(5)(b) unless the catering is an obligatory part of the event structure. Always obtain a written legal opinion from your CA on ITC eligibility for each event type before filing the claim.

Q2: What is the GST rate on event management services in India?

Event management services in India attract GST at 18% under SAC code 998590. This applies to the agency’s service fee for planning, coordinating, and executing events. Individual service components — accommodation, transport, catering, AV production — each attract their own GST rates as specified by the GST Council. In a Single-Window Billing model, the agency’s invoice should clearly distinguish between the management fee (18% GST) and the pass-through cost components with their respective rates.

Q3: What is the difference between a composite supply and a mixed supply in event billing?

A composite supply is a bundle of goods or services where one component is the principal supply and the others are naturally ancillary — for example, a conference package where the principal supply is the venue hire and accommodation, with meals and AV being ancillary. The entire composite supply is taxed at the rate of the principal supply. A mixed supply is a combination of two or more independent supplies that could be sold separately, bundled together for a single price. Mixed supplies are taxed at the highest GST rate applicable among all components. This distinction is critical in event billing because an incorrectly classified supply can result in under-taxation, over-taxation, or invalid ITC claims — all of which create audit exposure.

Q4: Is GST applicable on events held outside India by Indian companies?

When an Indian company organizes an event outside India, the services consumed abroad are generally outside the scope of Indian GST. However, the Indian event management agency’s service fee — for planning and coordinating the event from India — is subject to Indian GST at 18%. The foreign vendor costs (hotel, local transport, international entertainment) are not subject to Indian GST but are also not eligible for Indian ITC. In a Single-Window Billing model, the invoice should clearly segregate the Indian GST-applicable management fee component from the foreign cost pass-through component to ensure accurate tax treatment on both sides.

Q5: How does Single-Window Billing help during a GST audit?

During a GST audit, the tax department examines the accuracy of your ITC claims by cross-referencing your purchase invoices against supplier GSTR-1 filings. With Single-Window Billing, your audit file contains one primary invoice from a single GST-registered event management agency, rather than 20+ invoices from various vendors with varying compliance histories. This dramatically simplifies the audit process. The event management agency’s invoice, supported by the post-event cost reconciliation report and sub-vendor summary, provides a clean and complete audit trail. Any queries from the GST department can be addressed by producing the agency’s documentation package rather than chasing 20 individual vendors for their filing records.

Q6: What should a GST-compliant event invoice include?

A GST-compliant event management invoice must include the following elements: the supplier’s full legal name, registered address, and valid GSTIN; the recipient’s legal name, registered address, and GSTIN; a unique invoice number and date; a clear description of each service provided with the applicable SAC code; the taxable value of each service line item; the applicable GST rate and GST amount (CGST/SGST for intra-state or IGST for inter-state transactions) for each line item; the total invoice value inclusive of all taxes; and the place of supply, which is critical for determining whether IGST or CGST/SGST applies. Any invoice missing these elements is non-compliant and the ITC claim based on it can be rejected during an audit.

Conclusion: Single-Window Billing is Not a Convenience — It is a Compliance Imperative

The complexity of GST compliance in corporate event management is not widely understood until something goes wrong — a rejected ITC claim, a GST audit notice, a TDS disallowance, or a GSTR-2A mismatch that takes months to resolve.

Single-Window Billing transforms this complexity from a liability into a non-issue. By consolidating all event vendor payments, GST compliance, TDS management, and post-event reconciliation into a single structured billing relationship, it protects your organization’s tax position, saves your finance team significant administrative burden, and gives your procurement team complete cost transparency on every event.

The question to ask in your next event RFP is not just “what is your per-head cost?” It is “what does your billing model look like, and how do you protect my GST compliance?” The answer to that second question will tell you more about the quality of the agency than any portfolio presentation ever could.

Ready to simplify your event billing and GST compliance? Encore Events Global offers 100% Single-Window Billing on every event we manage — domestic or international. One invoice, full ITC support, complete sub-vendor transparency, and a post-event reconciliation package your CA will appreciate. Talk to our team today.

About Encore Events Global

Encore Events Global is a premier event execution and production partner headquartered in Mumbai, India. Founded in 2010, the company specializes in Corporate MICE & Offsites, Brand Activations, Destination Weddings, Exhibition Design, and large-scale Live Event Production. With a pan-India presence, owned warehousing in Mumbai and Delhi, and global partner networks in Dubai and Singapore, Encore Events Global engineers experiences — not just events.

Office: 108, Richa Industrial Estate, Off New Link Road, Andheri West, Mumbai 400053

Phone: +91 98332 64509

Email: info@encoreeventsandpromotions.com

Website: encoreeventsglobal.com